Audit practice is increasingly shaped by a combination of established auditing standards and rapidly evolving technology. While perspectives differ on the role of automation and AI in audit workflows, all approaches must ultimately be evaluated against PCAOB and AICPA requirements for audit evidence, documentation, and professional judgment.

This article examines how traditional audit procedures and AI-enabled tools compare in practice, and where each fits within the current regulatory framework.

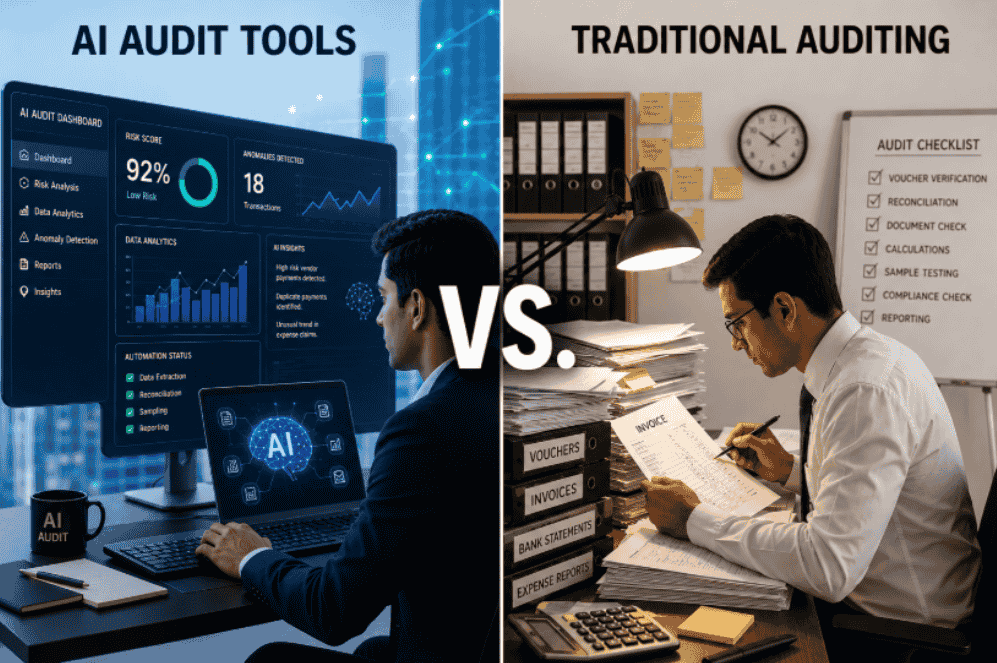

What traditional auditing actually delivers

Traditional audit techniques have proven their value in providing financial assurance for well over a hundred years. The foundational principles remain sound: professional skepticism, factual conclusions, and personal interaction with client documentation.

A seasoned auditor provides context-specific knowledge that no computer system can. Being able to read behavioral signals from client interviews, understand confusing accounting disclosures, and have specialized knowledge in a particular field are human traits.

In accordance with AU-C Section 500 on audit evidence and AU-C Section 230 on audit documentation, the gathered evidence must support conclusions subject to regulatory review. The traditional auditing system has been built on exactly these principles.

Under existing standards, AI-generated analyses do not automatically constitute sufficient audit evidence; auditors remain responsible for evaluating reliability, relevance, and completeness.

Auditors still spend a substantial portion of their time on repetitive manual activities such as data preparation, reconciliation, and documentation. It makes it difficult for them to engage in higher-order analytics. Traditional auditing, based on rigid rule sets and expert judgment, struggles with accuracy and generalizability when applied to high-dimensional, complex financial data.

The Wirecard scandal illustrated how significant fraud can remain undetected despite traditional audit procedures, particularly when falsified documentation and third-party confirmations are involved. The auditors failed to detect over $1.9 billion in financial fraud, contributing to the bankruptcy of a company once valued at more than €20 billion. A manual sample-based approach could miss information revealed only through population-level analysis.

Scale is a structural weakness of manual auditing. It was designed for a world where transaction volumes were manageable. That world no longer exists.

What AI audit tools actually do

The phrase “AI auditing tools” covers a wide range of capabilities. Precision matters here.

In its basic form, automated audit software handles document processing, matching, and exception identification. The purpose of these features is to improve efficiency through faster cycle times and reducing time spent on repetitive administrative tasks

At a more sophisticated level, AI-driven auditing uses machine learning to identify exceptions across the entire population of transactions, not just samples. It finds anomalies and exceptions that need further investigation. AI may improve anomaly detection at scale, but sophisticated fraud schemes involving collusion, fabricated evidence, or management override can still evade automated systems.

AI can process information much faster than humans, automate routines, identify unusual patterns, flag anomalies, and support risk assessment. It is this potential that regulators now officially acknowledge.

According to a Gartner survey, 41% of chief audit executives are already using or plan to use generative AI in their audit work. A McKinsey survey found that 65% of organizations are now regularly using generative AI — nearly double the prior year’s figure.

These figures suggest that AI adoption in audit and finance functions is moving beyond experimentation and into broader operational use.

According to the 2024 Audit Survey Report from the Thomson Reuters Institute, 41% of firms report their top challenge is meeting client expectations while maintaining high service standards. AI in auditing directly addresses this constraint — not by lowering standards, but by expanding capacity within them.

The regulatory position

CPAs cannot adopt technology in isolation from the standards that govern their work. The regulatory landscape for AI in auditing has been significantly clarified.

The PCAOB released a publication summarizing its observations on integrating generative AI into audits and financial reporting, as part of a broader research project assessing whether changes to PCAOB standards or other regulatory actions are warranted.

The PCAOB’s Technology Innovation Alliance Working Group delivered its recommendations in May 2024, identifying the responsible integration of AI into audit practice as a strategic priority.

The position is clear: the use of technology in conducting an audit cannot replace human judgment and understanding. Professional judgment and skepticism are equally important when using technology, and must be performed by people, not machines.

This is the regulatory framework against which the problem of traditional and AI auditing must be considered. Neither traditional nor AI-assisted auditing alone fully satisfies the demands of modern audit environments.

Where each approach fails

Traditional audit methodologies were developed in an environment with lower transaction volumes and more centralized documentation. In highly digital financial ecosystems, sample-based testing may not always identify anomalies distributed across large transaction populations. At the same time, AI-assisted auditing introduces its own risks related to model governance, data quality, explainability, and overreliance on automated outputs.

There has to be some form of governance involved with an automated auditing process using artificial intelligence. Machine learning algorithms designed with bias will produce biased results. AI systems also introduce governance concerns related to training data quality, explainability, cybersecurity, and model drift over time

The failure modes are different. Neither is trivial.

AI vs manual auditing: the comparison

| Dimension | Traditional Auditing | AI Auditing Tools |

| Coverage | Sample-based | Full population |

| Speed | Weeks to months | Hours to days |

| Error exposure | Human misstatement risk | Model/data risk |

| Judgment capacity | High | Low |

| Regulatory compliance | Established (PCAOB AS 2101, AICPA AU-C 315) | Governed under existing auditing standards, though no AI-specific auditing standard currently exists |

| Fraud detection | Limited by scope (see PCAOB AS 2401) | Stronger on volume patterns |

| Scalability Confirmation procedures | Low Manual, interception-prone (see PCAOB AS 2310) | High Digital, documented, tamper-resistant |

The comparison above is not an argument for wholesale replacement. It is a map of complementary strengths.

AI vs manual auditing is the wrong frame. The relevant question is: where does each approach add the most value, and how should they be combined?

The hybrid model

Leading audit practices are not choosing between AI and manual methods. They are restructuring workflows to apply each where it performs best.

Automated audit software handles data ingestion, reconciliation, and exception generation. Auditors apply judgment to exceptions, design procedures governing AI outputs, and maintain the professional skepticism that standards require. As adoption expands, firms should also expect increasing scrutiny from regulators, audit committees, and inspection bodies regarding how AI-generated outputs are validated, documented, and supervised.

Confirmation processes — historically among the most fraud-exposed steps in an audit — are increasingly handled through secure digital platforms with documented audit trails.

PCAOB board members have argued that the PCAOB should serve as an engine catalyzing innovation in public company auditing, with audit quality as the end goal. The hybrid model is precisely what that vision implies.

Conclusion

The evidence does not support a winner-takes-all outcome. Both methods will be needed to fill the needs of the field.

In considering the shift from one form of auditing to the next, the key questions that arise are which technologies work in this space, and which systems are to be trusted?

AuditConfirm was developed specifically for this reason. With the help of AuditConfirm, an audit confirmation platform designed to support audits conducted under PCAOB standards, users receive fast, automated audit confirmation in one of the most important and vulnerable areas of external audit. This does not mean that AuditConfirm replaces auditor judgment, but rather supplements it to ensure accuracy and compliance with standards.

The future of auditing lies in a balanced use of both techniques.

Disclosure: This article was posted by AuditConfirm — an audit confirmation platform designed to support audit procedures performed in accordance with PCAOB standards.To read more, you can refer to the PCAOB Generative AI Spotlight and the AICPA resources related to audit data analytics, along with Caseware’s 2024 State of Internal Audit Trends Report.

FAQs

AI audit tools are software programs that use AI and automation to analyze data and identify deviations in accounting entries. Traditionally, auditing involves examining accounting data through sampling. The main difference between the two approaches is the size of the analysis they can provide.

While AI in auditing is allowed, there are no standardized guidelines. The PCAOB’s involvement in this matter is evident in the formation of the Technology Innovation Alliance Working Group and the publication of the Generative AI Spotlight. Current standards like AS 2310 and AU-C 500 will still apply to AI outputs.

Traditional auditing vs AI auditing comes down to where time is spent. Manual auditors spend the bulk of their hours on data gathering and reconciliation. AI auditing tools shift that time toward exception review and professional judgment — the work that actually requires a CPA.

Audit software does all the processing, recognition, and recording. Automated software, however, is devoid of professional skepticism, consideration of context, and approval of findings. The PCAOB standard clearly states that technology helps auditors make decisions; however, technology does not make the decisions.

The difference between AI-based and traditional audits is best exemplified in the confirmations process. Traditional confirmation techniques utilize paper, which is prone to delay and can be intercepted and altered. Digital confirmation platforms can help firms perform confirmation procedures in alignment with PCAOB AS 2310 requirements, filling in the gaps that have existed since the beginning of manual processes.